On the Spot: Are a ‘Stag and Flation’ Lurking?

May 07, 2024

Market run-through

The markets seem fixated on when the Federal Reserve will start to drop interest rates in the US. Certainly, Chairman Powell was slightly more dovish in his press conference after the FOMC meeting than many had anticipated. Some traders opined that Jay Po had had a sneak preview of last Friday’s Non-Farm Payrolls figure, and after the number came in moderately weaker than analysts had predicted, this view gathered strength. As the saying goes, one swallow doesn’t make a summer, and I think he will still need to see at least another couple of data runs before a rate cut. On the basis that the economy is at last showing signs of some weakness, it looks like September is the month for a cut. But, and as always, there is a but. US Money Supply expanded again last month, more often than not a sign of impending inflation and possibly Stagflation.

On the subject of money supply and stagnation, the UK is also showing signs that we are heading in a similar direction. Last week, Lord King of Lothbury, former Governor of the Bank of England was scathing in his criticism of the incumbent at the Bank of England and their lack of understanding of money supply. Whether Governor Bailey has taken on board his criticism, let alone Ben Bernanke’s, it is too early to say; however, we get to hear his views on Thursday after the MPC’s monthly meeting. With the economy spluttering along, he would dearly love to light a fire under it and drop interest rates. Still, inflation is not dead, and upcoming figures may contain some unpleasant surprises. Indeed, the UK’s money supply is still expanding, which should certainly give him pause for thought. Those hoping for an early cut are almost sure to be disappointed with probably a tweak of the Old Lady’s forward guidance being the most positive sign for them, leaving the end of summer as the most likely month for rate cut action.

Richard Matthews, Head of FX and Payment Partnerships

Chart of the week

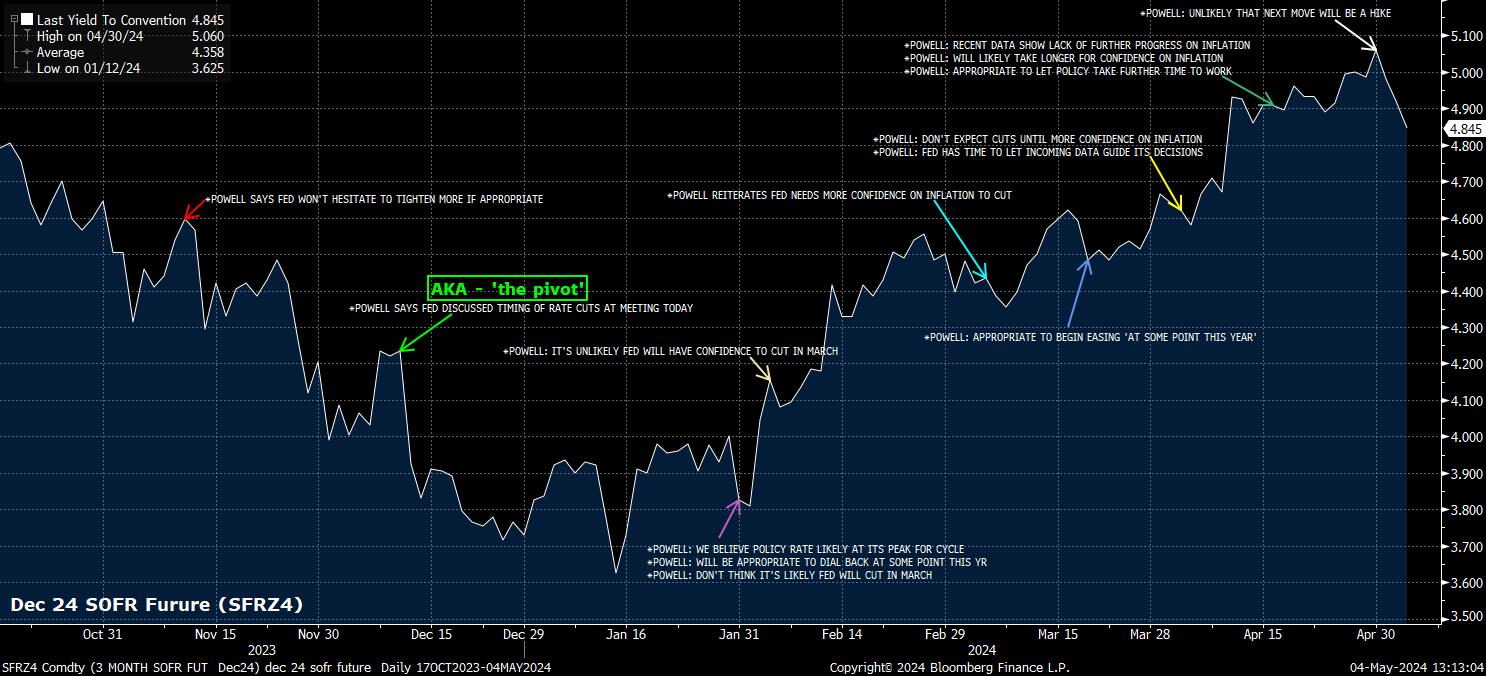

Last week’s highlight was, undoubtedly, the latest FOMC policy decision which, while seeing policymakers issue an almost identical statement to that released after the March confab, contained two factors which should maintain the bullish risk backdrop. Firstly, on the balance sheet, the Fed more than halved the cap on the pace of Treasury run-off, heading off potential funding issues or stresses within the financial system, ensuring that liquidity should remain plentiful. Secondly, Chair Powell himself, at the press conference, noted explicitly that it is “unlikely” the next move in the fed funds rate. Here, ‘unlikely’ is code for ‘never going to happen’, with the policy response to stickier than expected inflation simply to hold rates steady for longer, rather than deliver any additional increases. Together, then, we have an FOMC that remain desperate to cut and one that is already improving liquidity conditions via the balance sheet. The ‘fed put’, clearly, is alive and well, and should see the path of least resistance on Wall St continue to lead higher for some time to come.

Michael Brown, Market Analyst at Pepperstone

Disclaimer: The views contained herein are not to be taken as a recommendation or advice. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. It is very important to do your own analysis before making any investment based on your own personal circumstances. You should take independent financial advice from a professional in connection with, or independently research and verify, any information that you find on ONE’s website and wish to rely upon, whether for the purpose of making an investment decision or otherwise. It should be noted that investment involves risks, the value of investments may fluctuate in accordance with market conditions and investors may not get back the full amount invested.

Not all ONE services may be available to UK customers.