The Ultimate Guide To Cross-Border Payments

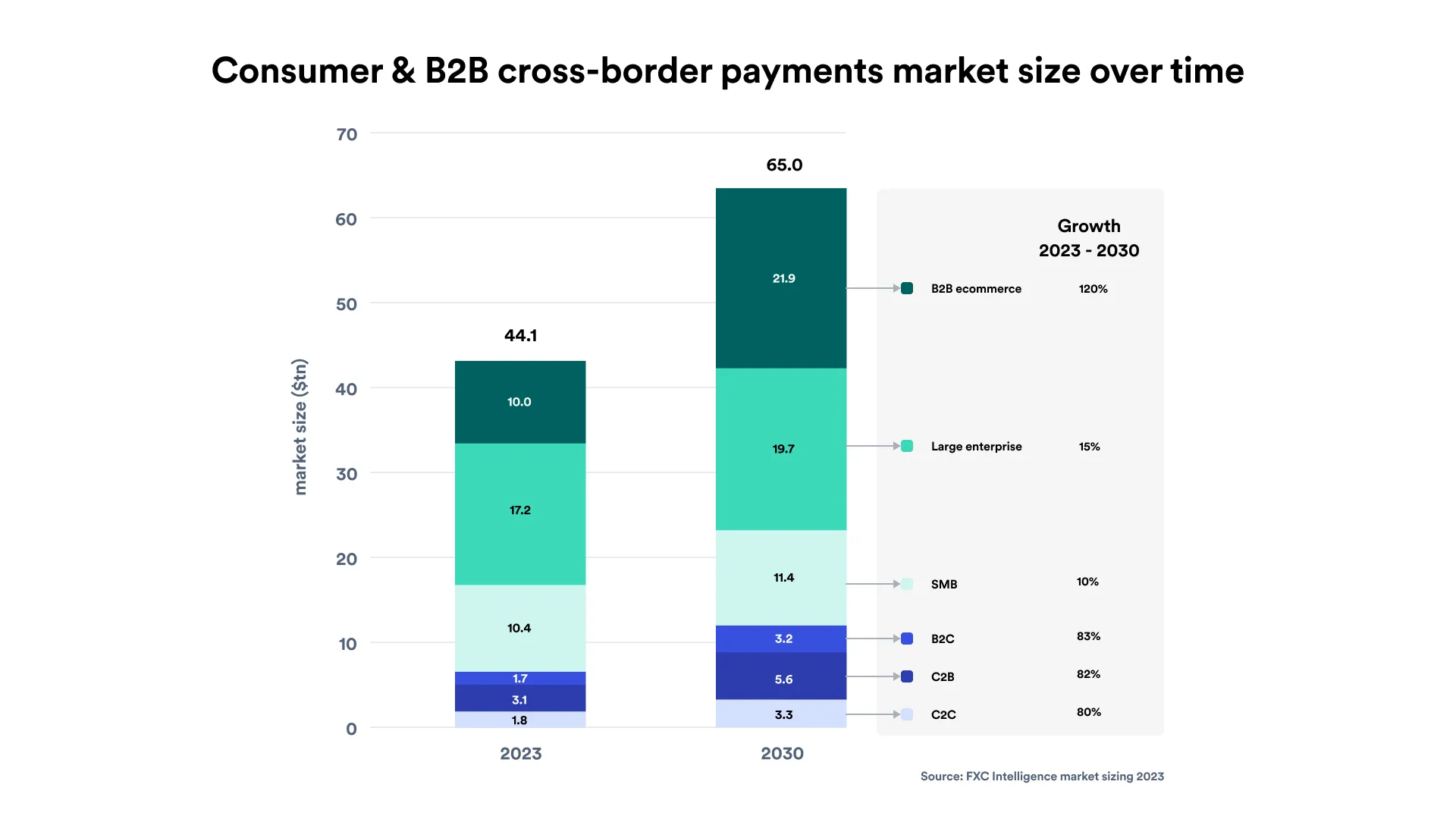

Cross-border payments are on the rise. According to the Bank of England, the value of cross-border payments is forecast to increase from almost $150tr in 2017 to over $250tr by 2027. Making international payments can be a challenging and expensive process. However, with the right payment partner, you can alleviate these obstacles and unlock the potential for international expansion. Read on to find out what cross-border payments are, how to make one, how long they take, and how payment platforms like ONE can streamline your payment process.

What are cross-border payments?

Cross-border payments cover any payment or transaction made where the customer is located in a different country than the recipient. In a world where globalisation is expanding rapidly through eCommerce and international B2B payments, it is vital for business owners to have a good understanding of cross-border payments and where they fit into their own business transactions.

In this guide, you will find:

- How does a coss-border payment work?

- The types of cross-border payments

- Factors affecting cross-border payments

- Tips for efficient cross-border payments

- Challenges in cross-border payments

- Conclusion

How does a cross-border transaction work?

Cross-border transactions are a lot more complex than domestic transactions, as things like exchange rates, transaction fees and other complications are introduced. You’ll also find that for each layer of financial institution or entity that your payment has to go through, it will take longer and become more exposed to risk.

Types of cross-border payments

There are many cross-border payment types such as, inward remittances, outward remittances, cross-border e-commerce payments and cross-border business payments. It’s useful for business owners to become familiar with all types of cross-border payments.

Inward Remittances

Inward remittances are cross-border payments that are sent from a foreign country into the recipient’s home country.

An example of an inward remittance might be a person working abroad, who sends regular payments to their family at home. In the same sense, if a foreign company pays for goods or services from a domestic company, that would be considered an inward remittance.

Inward Remittances can be a massive boost to a country’s economy, although it is worth bearing in mind that some countries have specific regulatory or reporting requirements surrounding inward remittances.

Outward remittances

Outward remittance is the process of transferring money to another country, whether it be as a person or business.

These types of payments are also subject to various regulatory and reporting requirements, which may differ from country to country. You may also be charged or incur a fee during an outward remittance. Foreign transaction fees, currency conversion fees and wire transfer fees (among others) may vary depending on the payment service provider and the transaction amount.

Nonetheless, outward remittances make up a large portion of international trade, commerce and investments abroad.

Cross-border e-commerce payments

E-commerce cross-border transactions refer to any transaction made online when goods and services are purchased from a business based in a foreign country. This includes everything from purchases made on huge websites like Amazon or eBay to smaller online businesses that have the capability of operating internationally.

Cross-border business payments

Cross-border business payments are transactions where businesses from two different countries pay each other for goods and services. This typically happens through international wire transfers or payment platforms like ONE. Payments like these can be quite complex when factors like exchange rates, regulations, and compliance are introduced.

Factors affecting cross-border payments

Exchange rates

Exchange rates can greatly affect your cross-border payments, depending on how they sit at the time of your transaction.

Unfavourable exchange rates mean that you’ll need to pay more of your transactional currency when purchasing the foreign currency required for your cross-border payment. On the other hand, favourable rates mean you’ll pay less upon exchange, helping you save money on that transaction.

Many businesses use strategies such as forward contracts or lock-in options, to keep exchange rates at a favourable level when the time comes to complete the transaction. This is a great way to manage costs when making international payments.

Fees

The chances of paying fees or charges when making international payments are generally much greater, and it is always worth checking with your payment provider to understand what fees may affect you.

There are a host of transaction fees that businesses and individual traders should be aware of, but some of the most common are:

Currency exchange fees: You may be charged this when converting your currency to another. This fee is heavily dependent on market conditions and the payment providing handling the transaction.

Transaction/processing fees: Your payment provider may charge a transaction/processing fee when processing the cross-border transaction. These fees are often dictated by the type of payment used, the amount of the transaction, and the payment providers themselves.

Receiving fees: You may be charged a fee for receiving a payment, depending on the payment provider. Usually, this fee is charged to the recipient separately, or the fee amount is deducted from the overall payment amount.

Intermediary bank fees: Additional fees may be charged if the payment needs to run through an intermediary bank. The fee amount can vary depending on elements like where the recipient lives, and what the intermediary dictates. Most banks charge a fixed amount when making an outgoing international wire transfer, with fees average $44.

Correspondent bank fees: Much like Intermediary Bank Fees, Correspondent Bank Fees may be charged when a payment runs through a correspondent bank. These fees are also subject to the correspondent bank, and recipient location.

How much time does a cross-border transaction take?

Typically, cross-border transactions take up to five days to be processed and received into an account, although other factors may affect that time such as payment rails and fraud prevention processes.

Blockchain payments

According to Fortune Business Insights, blockchain-based cross-border payments are gaining popularity, with the market expected to grow at a CAGR of 82.5% between 2021 and 2028. These transactions can be an effective way for businesses to make and receive payments globally.

Other factors

Be aware that factors such as bank holidays, weekends, and payment processing times all play a part in how long cross-border transactions take to complete. When making international payments, discuss with your payment provider whether these elements may affect you.

Regulatory requirements

Adhering to regulations is very important when making cross-border transactions, and businesses that do not adhere to them may face penalties or other legal ramifications.

The EU has established rules and regulations for cross-border payments, and SEPA (Single Euro Payment Area) payments require transparency on fees when payments are made between EU members.

When factoring in other regulatory requirements for both Europe and globally though, there are a number of regulations that you should discuss with your payment provider, to ensure that you are compliant:

- The AMLFC (Anti-Money Laundering and Financial Crime Institute) and the KYC (Know Your Customer) guidelines are required to verify the identity of customers to ensure that their cross-border payment isn’t financing illegal activities. Illegal activities could include laundering, financing terrorism, financial crimes and more.

- Sanctions and export control regulations: Payment providers must ensure that transactions with sanctioned countries are restricted. This also applies to sanctioned individuals and other entities as well.

- Regulations on foreign exchange: There may be rules on exchange rates, capital controls and more that you must adhere to when making international payments. Speak to your payment provider to ensure that both you and they are meeting regulations.

- Data privacy and user security regulations: Personal and financial data is heavily regulated. For example, 2FA (two-factor authentication), and 3D Secure 2.0 are both used globally to ensure that private data is kept as such.

- Reporting requirements and regulations: Certain types of international payments may need to be reported to government agencies and other regulatory bodies. This is a requirement for a large portion of financial institutions, who may monitor payments to ensure that no illegal activities are taking place.

Cross-border payment methods

International wire transfers

International wire transfers are a common method of cross-border payment and simply involve sending money electronically from one payment provider to another using the SWIFT network. Be aware of any fees and exchange rate fluctuations involved with this type of payment.

SWIFT options

When making a SWIFT International Wire Transfer, take note of the different options available when deciding who will pay transfer fees. The options are as follows:

OUR – Selecting the OUR option means you will pay the transfer fee before the transfer is initiated. The full transfer amount will then be delivered to the beneficiary.

BEN – The BEN option means that transfer fees are expected to be paid by the beneficiary, so any fees will be deducted from the amount that you are transferring.

SHA – If you select the SHA option, it is expected that the transfer fees will be shared. This means that some of the charges are expected to be paid before making the transfer (similar to OUR), and the rest is expected to be deducted from the amount you are transferring before it reaches the beneficiary.

When making international wire transfer payments, you will need access to your IBAN (International Bank Account Number), which provides extra information so they can identify you.

Credit cards

Credit Cards can be utilised for cross-border payments, but be aware of any fees that may come with using one. Also be aware that merchants may not accept credit cards from certain countries, so be sure that it is a viable option before you attempt a payment.

Online payment platforms

You can use payment gateway systems to send and receive money internationally, and while convenient and easy to use, these platforms may also charge high fees.

Blockchain

The blockchain is slowly being adopted by financial institutions across the world for its security and transparency. It also allows for real-time payments thanks to fewer negotiations entering the payment process and requires a minimal fee for the transaction – a large point of contention surrounding SWIFT payments.

Making payments through the Blockchain also makes it much more difficult to tamper with information, as each piece of information is linked with the previous block. On top of this, due to the decentralised nature of the Blockchain, the flow of information between clients across different countries and jurisdictions can be prevented, allowing for greater security.

Tips for efficient cross-border payments

Plan ahead

Planning ahead when making cross-border payments is essential to helping you make the most of your transaction. If viable, make a forward contract between yourself and the recipient to keep costs favourable to you.

Choose the right payment method

Choosing the right payment method is a great way to ensure that you keep any fees or charges to a minimum. Consider looking at all the options to see which ones work best for your business.

Consider exchange rates and fees

Exchange rates fluctuate daily to align with financial changes locally and globally. Having a good idea of how exchange rates may change can make all the difference in whether you make a payment early or not.

Fees can also be a thorn in the side of a potential transaction. Save money on your transaction by considering what method you want to use to send the payment and what fees are attached to the exchange.

Verify the recipient’s details

When making a cross-border payment, always verify the details of the recipient.

Some countries have very specific regulations that must be complied with, where payments can only be sent to certain account types, individual traders or businesses. Making sure you have the correct details can prevent delays and other issues arising through non-compliance.

Verifying the recipient details also helps to prevent your money going to potentially fraudulent parties. Scammers using fake accounts, or accounts belonging to others can be very damaging to businesses and individual traders, who believe they are sending money to a legitimate account. Always make sure the account you are sending money to is real.

ONE has a built-in confirmation of payee tool built into our platform for ultimate peace of mind. When you make a one-time or recurring UK sterling payment to someone for the first time, we’ll verify that the name and account details match what’s registered with their bank.

Keep records

Most businesses will keep records of their transactions, and it’s no different for cross-border transactions too.

Keeping a record not only helps you understand where and when your money has been moved, but also allows you to provide evidence if you are a victim of fraud, or run into issues surrounding regulations.

What are the challenges with cross-border payments?

Despite the benefits, cross-border payments also come with some challenges, including:

Security risks

Cybersecurity is very important for payment providers because varying regulations between countries can leave payment systems open to hacking, especially if that country’s security and access policies are less stringent.

In the circumstance that your money is lost while making a cross-border payment, there are also no guarantees that your payment provider can recover it. Therefore, it is very important that you understand where your money is going, and the risks involved with sending money internationally.

Currency risks

As previously discussed, exchange rates between countries can fluctuate quickly and are subject to both political and economic events around the world.

When working with international businesses and individual traders, consider the exchange rate of that country and whether you need to increase prices to make up for the conversion costs.

You should also be aware that a delayed payment can result in a different exchange rate than what was expected.

Technology limitations

The technological landscape around cross-border payments shifts constantly to meet new methods and currencies, and reduce the risk of cybercrime. There are still many limitations to overcome though with current methods that businesses and individual traders should be aware of.

Differing payment systems used by financial institutions can also not work well together, creating friction on cross-border payments which can slow down transactions and leave them open to security risks.

The future of cross-border payments

Cross-border payments are evolving rapidly, and it is worth understanding just how new technologies may improve your cross-border payment processes.

How Fintechs can solve cross-border payments

Fintech solutions are also growing rapidly, and utilise accounts in multiple currencies to help users make fast and secure international payments. Traditionally ‘high-risk’ industries benefit greatly from partnering with these solutions, as they provide a way for these industries to make payments without having to build layers of contingency banking.

Cross-border payments – in conclusion

Cross-border payments are changing quickly, and changes to the landscape will likely be seen within this decade.

Always consider these points when making international payments:

- As a business or individual trader, always be sure to speak to financial advisors and service providers, so you understand exactly what regulations and fees you may face.

- Keep an eye on exchange rates and predictions, which fluctuate often. These will dictate when the best time to make a payment is.

- Verify the details of your recipients to lower the risk of sending money to a fraudulent account.

- Keep track of all your records so payments can be traced and evidence provided in the event of fraud or any other payment-related issues.

- If you make frequent cross-border payments, consider looking into new technologies like the blockchain to make your transactions quicker and safer.

- Utilise fintech solutions if they are applicable to your business. These solutions can provide multiple methods of payment while allowing full transparency, and offer multi-currency accounts, batch payments, and more.